From Hype to Utility: Marketing’s Great AI Pivot in 2026

The advertising industry has officially entered a new phase of maturity regarding Artificial Intelligence. According to the 2026 H2 Market Report released by Mediaocean, the era of viewing AI as a monolithic, all-encompassing "workflow transformer" is receding, replaced by a more pragmatic, surgical approach to the technology. While investment in AI-driven media channels is skyrocketing, the perception of AI’s immediate, broad-scale impact on daily operations has cooled, suggesting that marketers are pivoting from broad experimentation to specific, high-utility use cases.

The Main Facts: AI Media Takes the Lead

The latest industry research from Mediaocean, marking the tenth installment in its influential bi-annual series, reveals a stark paradox: marketers are pouring record capital into AI-integrated media while simultaneously tempering their expectations regarding AI-driven organizational transformation.

The report, which synthesized data from 312 marketing professionals across brands, agencies, and tech providers, identifies AI media—defined as advertisements served on AI agents and platforms—as the fastest-growing investment category. A remarkable 60% of marketers plan to increase their spending in this area during the second half of 2026.

Conversely, the belief that AI is causing a "major workflow transformation" has plummeted to 19%, down significantly from 28% in the previous period. This suggests a transition from the "discovery phase" of AI to an "operational phase," where the technology is being utilized for granular tasks rather than being viewed as a panacea for agency-wide efficiency.

Chronology: A Decade of Digital Evolution

Mediaocean’s research series, which began in late 2021, has tracked the digital advertising landscape through 6,400 total respondents. To understand the current trajectory, one must look at the historical progression of these trends:

- Late 2021: The inaugural survey sets the baseline for the post-pandemic digital advertising boom.

- 2024–2025: AI begins its ascent, consistently ranking as the top consumer trend for four consecutive reporting periods.

- May 2025: E-commerce and CTV (Connected TV) reach peak excitement, while AI adoption begins its climb.

- November 2025 (H1 2026 Data): AI media surpasses search in planned investment growth for the first time in the series’ history, signaling a fundamental shift in media buying.

- May 2026: The most recent survey confirms the acceleration of AI adoption in data analysis (rising to 50%) and the decline of manual spreadsheet-based workflows.

- June 16, 2026: Official publication of the 2026 H2 Market Report.

- July 14, 2026: A scheduled industry webinar featuring key experts, including Mediaocean CMO Aaron Goldman, to dissect the implications of these findings.

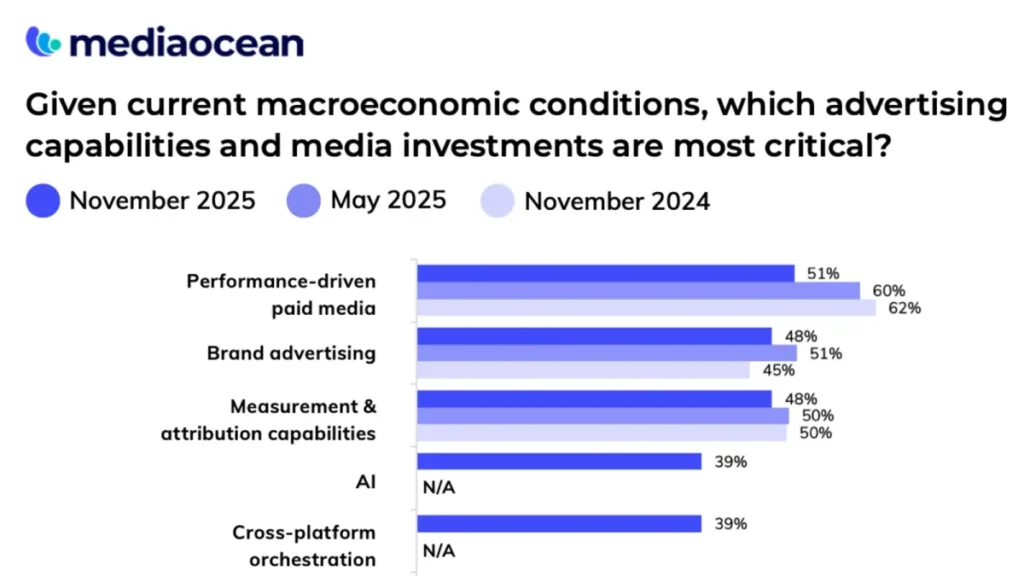

Supporting Data: Where the Capital is Flowing

The report provides a granular breakdown of budget allocations, painting a picture of an industry moving toward high-performance, automated channels while retreating from traditional, manual-heavy media.

Channel Spend Intentions

CTV and digital display/video are currently leading the charge, with 63% of marketers planning to increase their investment in both. Social platforms trail closely at 61%. Perhaps most notably, AI media has firmly established its dominance, with 60% of marketers planning to increase their budget for the second half of the year.

In contrast, traditional media remains in a state of contraction. Print leads the decline, with 49% of marketers planning to decrease spend, followed by local and national television, which continue to struggle against the tide of digital-first, data-driven programmatic buying.

Generative AI Use Cases

The utility of AI is becoming increasingly specialized. Data analysis has emerged as the clear winner, with 50% of marketers now using generative AI for this purpose, up from 43% just six months prior. Other growth areas include creative development and personalization, which have seen year-over-year adoption increases of over 50%.

Interestingly, the report highlights a sharp decline in technical AI applications. Website development and software coding tasks performed by AI have fallen to 6% and 8% respectively, suggesting that the initial hype surrounding AI as a replacement for technical development was premature or misplaced.

The "Orchestration" Disconnect

The report highlights a significant "Orchestration Gap." While 86% of respondents agree that cross-platform orchestration is "important" or "extremely important," a mere 10% have achieved a fully unified system. The majority (48%) describe their environment as "partially unified," hampered by significant silos that prevent cohesive cross-channel measurement.

Official Responses: Moving from Experimentation to Execution

Aaron Goldman, CMO of Mediaocean, views these findings as a maturation of the marketing sector. "The question now is how AI gets operationalized across planning, activation, measurement, and optimization," Goldman noted in his analysis of the report. "What this research shows is that marketers are moving beyond experimentation and looking for practical ways to connect intelligence with execution."

This move toward operationalization is supported by the industry’s departure from manual workflows. The report notes that 35% of marketers are actively transitioning away from spreadsheet-heavy processes toward API-driven automation. This shift is essential to addressing the primary barrier to AI adoption: data quality and integration.

According to respondents, the top hurdles are:

- Data Quality/Access Issues (42%)

- Difficulty Connecting AI Insights Across Multiple Systems (41%)

- Brand Safety or Compliance Concerns (40%)

These figures illustrate that the challenges of 2026 are no longer about the lack of AI capability, but rather the infrastructure required to support it.

Implications: The Road Ahead for 2026 and Beyond

The 2026 H2 Market Report serves as a sobering roadmap for the remainder of the year. The primary implication is that "AI-first" is no longer a marketing slogan; it is becoming a technical requirement for survival. However, the data also serves as a warning against over-automation.

Infrastructure Over Ideation

Marketers who spent 2024 and 2025 focusing on the "what" of AI are now being forced to confront the "how." With 56% of respondents citing "Fragmentation Across Platforms and Publishers" as their greatest concern, the second half of 2026 will likely be defined by a focus on infrastructure investment. Companies will be prioritizing ad tech stack interoperability over experimental innovation budgets, which have fallen from 22% to 13% over the last year.

The Human-AI Equilibrium

The decline in the perception of AI as a "major workflow transformer" is not a sign of failure; it is a sign of normalization. As AI becomes embedded into tools like Mediaocean’s NIVO AI—which has reported 90% workflow efficiency gains in pilot programs—the technology is fading into the background. It is becoming a utility, similar to electricity or high-speed internet, rather than a headline-grabbing event.

The Privacy Conundrum

Finally, the rise in the importance of privacy (up 33% since May 2025) suggests that as marketers become more sophisticated in their use of data, they are becoming equally concerned about the regulatory and signal-loss environment. The decline in concerns regarding third-party data loss—down from 34% to 21%—suggests that the industry has either accepted the "cookieless" reality or has successfully pivoted to first-party data strategies.

As the industry prepares for the July 14 webinar, the overarching takeaway is clear: the advertising sector is consolidating its gains. The frantic, broad-spectrum investment in AI is giving way to a more disciplined, integration-focused strategy that prioritizes cross-channel orchestration and measurable, bottom-funnel performance. For the remainder of 2026, the winners will not necessarily be those with the most AI, but those with the most integrated, reliable, and compliant AI infrastructures.